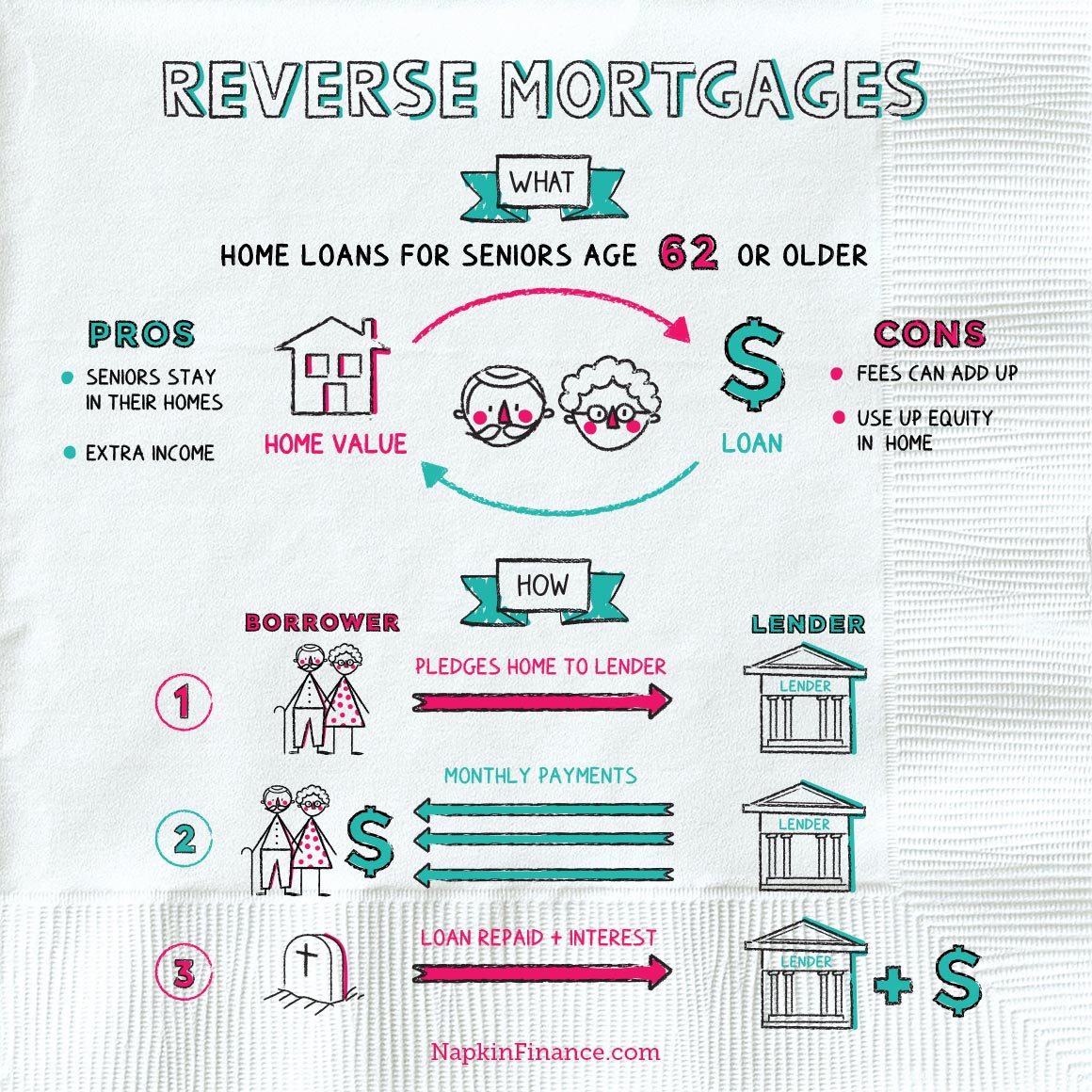

One of the most popular types of reverse home mortgages is the House Equity Conversion Home Loan (HECM), which is backed by the federal government. Despite the reverse home loan concept in practice, certified property owners may not be able to borrow the entire value of their house even if the home loan is paid off.

Homeowners are most likely to get a higher primary limit the older they are, the more the property deserves and the lower the rate of interest. The amount may increase if the debtor has a variable-rate HECM. With a variable rate, choices include: Equal regular monthly payments, supplied a minimum of one debtor lives in the residential or commercial property as their main home Equal month-to-month payments for a set duration of months concurred on ahead of time A credit line that can be accessed till it runs out A mix of a credit line and fixed regular monthly payments for as long as you live in the house A mix of a credit line plus fixed regular monthly payments for a set length of time If you select a HECM with a set rates of interest, on the other hand, you'll get a single-disbursement, lump-sum payment.

Supplementing retirement income, covering the cost of required home repair work or paying out-of-pocket medical costs prevail and acceptable usages of reverse home loan earnings, according to Bruce McClary, spokesperson for the National Structure for Credit Counseling."In each situation where routine income or available savings are inadequate to cover costs, a reverse home loan can keep senior citizens from turning to high-interest credit lines or other more costly loans," McClary says. Based upon the results, the lender could need funds to be set aside from the loan proceeds to pay things like property taxes, house owner's insurance, and flood insurance (if applicable). If this is not needed, you still could agree that your lending institution will pay these products. If you have a "set-aside" or you accept have the lending institution make these payments, those quantities will be subtracted from the amount you get in loan earnings.

The HECM lets you select amongst several payment alternatives: a single dispensation alternative this is just offered with a set rate loan, and typically offers less cash than other HECM choices. a "term" alternative fixed regular monthly money advances for a particular time. a "tenure" alternative fixed month-to-month cash advances for as long as you reside in your home.

Some Known Questions About What Banks Give Mortgages Without Tax Returns.

This option limits the quantity of interest troubled your loan, because you owe interest on the credit that you are using. a combination of regular monthly payments and a credit line. You might have the ability to change your payment choice for a small fee. HECMs typically offer you bigger loan advances at a lower total cost than exclusive loans do.

Taxes and insurance still must be paid on the loan, and your house needs to be maintained. With HECMs, there is a limitation on how much you can get the first year. Your lender will compute just how much you can obtain, based upon your age, the rates of interest, the worth of your house, and your monetary assessment.

There are exceptions, however. If you're considering a reverse home loan, search. Choose which type of reverse home mortgage might be ideal for you. That may depend upon what you want to finish with the cash (what is a non recourse state for mortgages). Compare the alternatives, terms, and fees from different lending institutions. Find out as much as you can about reverse home loans before you speak to a therapist or lending institution.

Here are some things to think about: If so, discover if you get approved for any low-cost single purpose loans in your area. Personnel at your regional Location Firm on Aging might learn about the programs in your location. Find the closest agency on aging at eldercare. gov, or call 1-800-677-1116.

Rumored Buzz on What Is The Interest Rate Today On Mortgages

You might be able to obtain more money with an exclusive reverse home mortgage. However the more you obtain, the greater the costs you'll pay. You also may think about a HECM loan. A HECM counselor or a lending institution can help you compare these types of loans side by side, to see what you'll get and what it costs.

While the home loan get rid of timeshare insurance coverage premium is normally the same from lending institution to loan provider, a lot of loan costs including origination fees, rate of interest, closing expenses, and servicing charges vary amongst loan providers. Ask a counselor or lender to explain the Overall Yearly Loan Cost (TALC) rates: they show the forecasted yearly typical expense of a reverse home mortgage, consisting of all the itemized expenses.

Is a reverse mortgage right for you? Just you can decide what works for your scenario. A counselor from an independent government-approved housing therapy agency can assist. However a sales representative isn't most likely to be the finest guide for what works for you. This is especially true if he or she acts like a reverse mortgage is a solution for all your problems, presses you to take out a loan, or has concepts on how you can spend the cash from a reverse home mortgage.

If you decide you require house enhancements, and you believe a reverse mortgage is the way to spend for them, search prior to selecting a specific seller. Your home improvement expenses consist of not only the price of the work being done but also the expenses and charges you'll pay to get the reverse home mortgage.

The Definitive Guide to Where To Get Copies Of Mortgages East Baton Rouge

Withstand that pressure. If you purchase those type of financial products, you could lose the cash you receive from your reverse mortgage. You do not have to buy any monetary items, services or financial investment to get a reverse mortgage. In fact, in some scenarios, it's unlawful to require you to buy other items to get a reverse mortgage.

Stop and contact a therapist or somebody you trust before you sign anything. A reverse mortgage can be complicated, and isn't something to hurry into. The bottom line: If you don't comprehend the cost or functions of a reverse home loan, leave. If you feel pressure or seriousness to complete the offer stroll away.

With a lot of reverse mortgages, you have at least three business days after near cancel the offer for any factor, without penalty. This is referred to as your right of "rescission." To cancel, you should alert the lender in composing. Send your letter by licensed mail, and ask for a return receipt.

Keep copies of your correspondence and any enclosures. After you cancel, the loan provider has 20 days to return any cash you have actually paid for the funding. If you suspect a rip-off, or that someone associated with the deal might be breaking the law, let the how to get out of a timeshare legally href="http://felixtyta155.trexgame.net/10-easy-facts-about-which-banks-offer-30-year-mortgages-explained">Click here for more therapist, lender, or loan servicer understand.